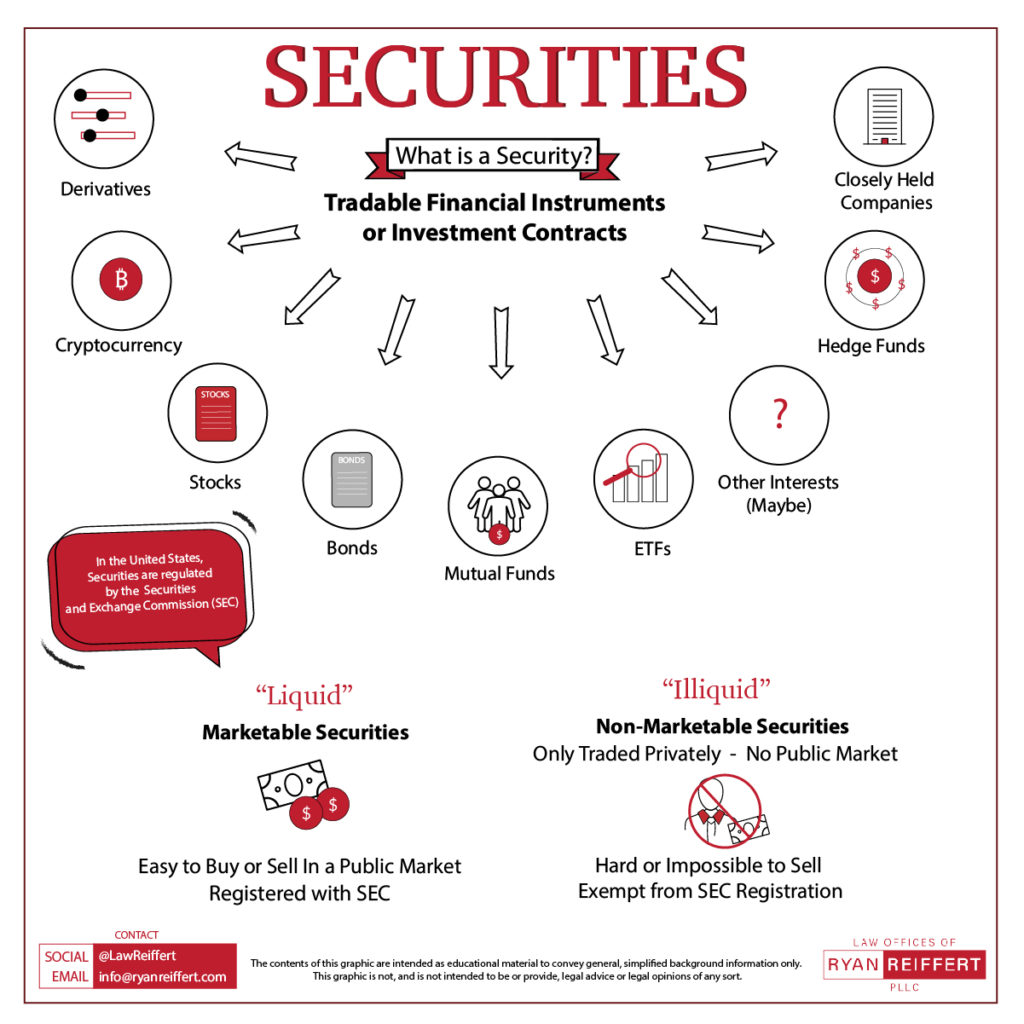

The landscape of securities laws and regulations is diverse and complex. In the United States, the field of securities law is quite broad, and has a number of subfields or subspecialties. The main fields within securities law include:

Public Securities Offerings.

This subfield covers offerings and sales of securities to the general public that are registered with the SEC under the Securities Act of 1933, including initial public (stock) offerings or “IPOs” as well as subsequent public offerings of either equity or debt. When you see a security listed on the NYSE or the NASDAQ (or the OTC/pink sheets), this is how their stock got there. Public securities offerings are typically complex and labor-intensive, involving multiple lawyers and accountants, as well as extensive interaction with the SEC.

Private Placements of Securities.

This subfield covers unregistered offerings and sales of securities on the private market. In order for an unregistered offering or sale to be legal, it must qualify for one of the SEC’s exemptions from registration. The maze of different exemptions and the rules for each is extremely complex, and it is easy to accidentally run afoul of the rules without proper legal guidance.

Securities Litigation/Enforcement Actions.

This subfield covers the civil or criminal suits that result when an issuer or person violates one of the rules discussed above, or another securities law. This litigation may be initiated by private individuals and companies, by the SEC, by the DOJ, or by a state securities regulator.

Restricted Securities/Securities Opinions.

Sometimes, securities issued by a company are classified as “Restricted” Securities and come with a restricted legend providing that they may not be transferred except under specific conditions. Often, in order for a transfer agent to process such a transfer, a letter from legal counsel will be required. This subfield covers those conditions

SEC Reporting and Compliance.

This subfield covers the public reports that must be filed from time to time by public companies in accordance with the obligations imposed upon them by the Securities Exchange Act of 1934.

State Securities Laws (“Blue Sky”) Compliance.

State securities laws are often referred to as “blue sky laws.” The expression gained currency when a Kansas Supreme Court judge referred to a speculative venture that had raised money through the sale of securities as having “no more basis than so many feet of blue sky” (i.e., there was nothing substantive to the speculative venture). For SEC-regulated offerings, state securities laws are often pre-empted and only a notification filing is required. Other times, they are not pre-empted, and compliance is required. We handle three of these five major areas – Private Placements, Blue Sky Compliance, Restricted Securities/Securities Opinions. While we have experience, and have consulted on, the other areas, they are not our main focus.

We handle three of these five major areas – Private Placements, Blue Sky Compliance, Restricted Securities/Securities Opinions. While we have experience, and have consulted on, the other areas, they are not our main focus.

We handle three of these five major areas – Private Placements, Blue Sky Compliance, Restricted Securities/Securities Opinions. While we have experience, and have consulted on, the other areas, they are not our main focus.

We handle three of these five major areas – Private Placements, Blue Sky Compliance, Restricted Securities/Securities Opinions. While we have experience, and have consulted on, the other areas, they are not our main focus.

Private Placements of Securities.

When might you need to retain an attorney to help with Private Placement? There is a simple answer to this question, as well as a more complicated answer. The simple answer is “any time you’re taking other people’s money and doing stuff with it” – and although this is admittedly vague, it covers the general idea. The more complicated answer is “it depends” – specifically, it depends upon how much money you are raising, from whom you are raising it, what you are going to do with the money (and what you actually do with the money), how you know the people from whom you are raising it, whether anyone else is involved in the transaction (and if so, what the other person’s role is), what promises or representations you have made to (or other sorts of agreements you have made with) the people you are raising it from, and some other related questions. Private Placement compliance advice may also often be sought in the context of granting employees stock options, incentive stock grants, etc. While this is slightly different from the case discussed above in that it does not involve the sale of securities in a private placement, it very much can still place the issuer or the issuer’s management in a bad position if the offering is not properly considered and structured. The penalties for failing to properly and fully comply with the correct exemption when attempting to effect a Private Placement can be steep, both in terms of exposure to liability from private lawsuits, as well as potentially civil and/or criminal consequences from the SEC, DOJ, and/or state securities regulators. Given the risks attached to launching a startup or investment type of venture, and the potential liability/downside risk associated with a failed venture, compliance with the securities laws is not optional. There are many other types of private securities deals, including the Private Investment in Public Equity or “PIPE” deal, wherein entities (often in syndicate) purchase unregistered (or private) shares of a publically traded company. These deals are very common in the private equity space, and with Qualified Institutional Buyers or (QIBs).Restricted Securities/Securities Opinions.

In some cases (often in private placements, but also in many public issuances as well) the securities issued will come with a “restrictive legend” directing that they may not be transferred or sold except in compliance with certain restrictions and conditions. One of those conditions is often an opinion of legal counsel that all other requirements for the removal have been met. In connection with the removal of a restrictive legend, an investigation or inquiry into the history and/or “provenance” of the securities will be undertaken, certain representations from the holders thereof will typically be required, and some level of verification of those representations may also be required. A qualified securities attorney will assess and fit all of these pieces together, evaluate the resulting picture, and then (if everything is in order) issue an opinion of legal counsel as required by the restrictive legend. Oftentimes this opinion will be provided by the issuer’s counsel, paid for by the stockholder. Other times the issuer’s counsel will decline to provide such opinions, and the stockholder will be required to seek out and retain his or her own counsel. Generally these types of opinions are referred to as Rule 144 Opinions, named after the SEC rule that provides the exemption permitting the public resale of restricted or control securities.Blue Sky Compliance/State Securities Laws.

State securities laws are often referred to as “blue sky laws” from a Kansas Supreme Court judge’s reference to securities sold in a speculative venture as having “no more basis than so many feet of blue sky”. In general, where an issuer complies with SEC requirements (whether through registration or through an exemption), the state blue sky laws will be pre-empted. In these situations, your securities attorney will most likely make a “notification filing” with the state(s) securities commission(s), stating that an offering was conducted, and due to compliance with SEC rules, it is exempt from any further state requirements. In other cases, a more fulsome filing with the state securities commission may be required in order to remain in compliance, which your securities attorney will be able to assist you with.