What is a Trust?

A trust is a legal entity that holds assets for many purposes. Trusts are very commonly used in the estate planning context; they are also used in the semi-overlapping context of asset protection strategies.

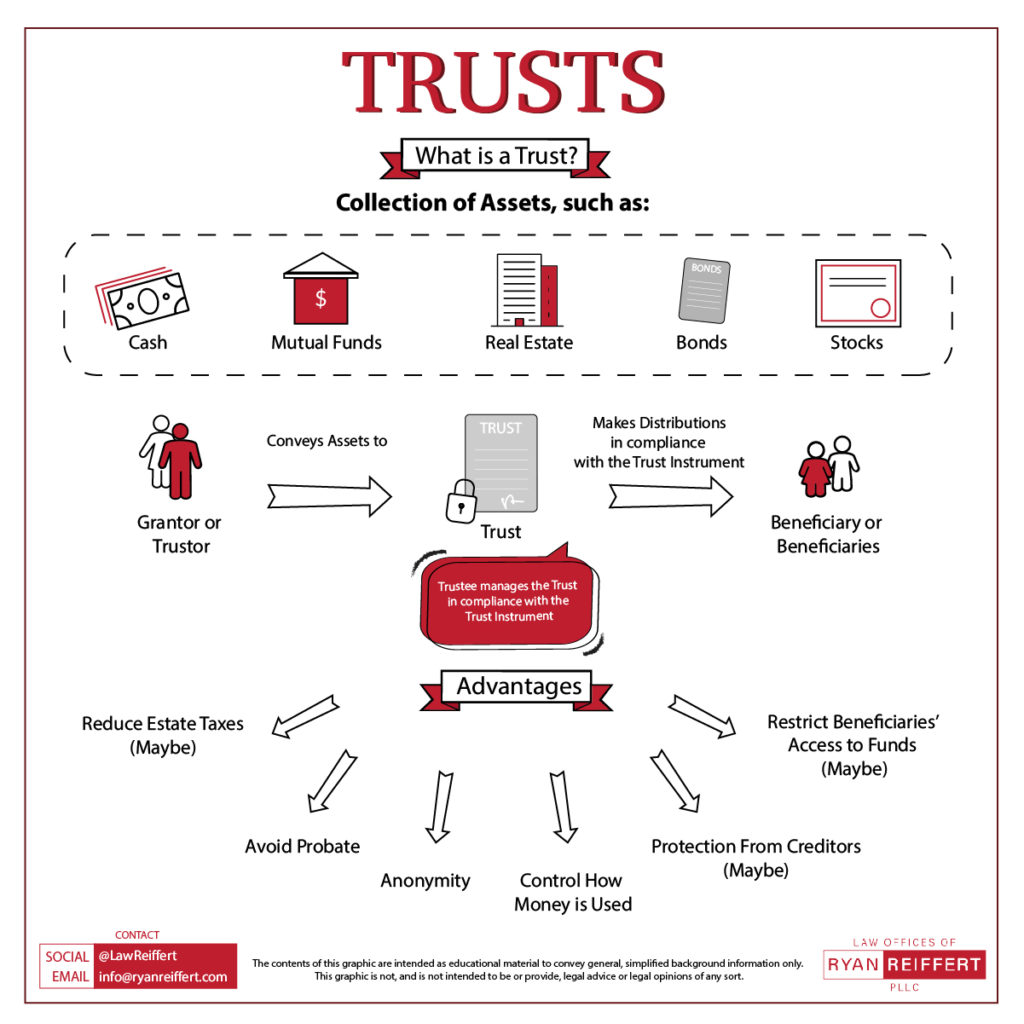

Infographic that answers the question: What is a trust?

A trust is designed to ensure that assets are managed and/or distributed to beneficiaries in accordance with the terms of the trust instrument. In the estate planning context, one of the main goals is to avoid the hassle and expense of the probate process and reduce the risk of the assets being encumbered by unnecessary taxes, as well as potentially the alienation of control with the goal of “protecting heirs from themselves” where there is a concern of, for example, financial irresponsibility, young age or immaturity, addictions, gambling, disability, and more.Relatedly, in the asset protection context, one of the main goals of a trust is to alienate control in order to exclude (at least partially) the trust from the reach of creditors, lawsuits, divorces, etc.

A trust may be created by an individual or a married couple as part of larger estate planning efforts or as part of a larger business-centric asset protection strategy. Do you notice a trend in both of the foregoing statements? A trust is generally NOT a magic bullet that will by itself accomplish all your legal aims. However, in conjunction with other devices, a trust IS a very powerful “tool in the toolkit”.

Wealthy individuals or business owners may also create trusts in order to preserve or grow wealth while minimizing or deferring taxes.

Trusts will generally involve three different parties:

Grantor. The person who creates the trust – referred to as the trustor, grantor, or settlor (in Texas, the terms are generally interchangeable and there is no appreciable difference among them)

Trustee. The person or entity who controls and manages the assets in the trust – this party is known as the trustee (there can be multiple trustees)

Beneficiary. The person(s) or entity(ies) who benefit from the assets in the trust – this person is called the beneficiary (there can be multiple beneficiaries).

In certain cases, these three roles can overlap, but the basic defining characteristic of a trust is a division between creation, control, and benefit. Those three characteristics are undivided in a “traditional” mode of outright property ownership (the legal term for this is fee, or fee simple, or fee simple absolute, ownership).

Once assets are placed into a trust, they are then owned by the trust itself. It is important not to take this decision lightly because, while the exchange of assets (of equal value) within a trust is relatively straightforward, the removal of assets from a trust can be more complicated depending upon the type of trust, as well as create unforeseen tax consequences They are then managed by the trustee to benefit the trust’s beneficiaries.

Many different “types” of trusts exist for various reasons, falling into categories that may blur, merge, and overlap (because a trust is extremely customizable depending upon the particular language of the trust instrument). These following four trusts are the ones that you are (probably) most likely to have heard of already:

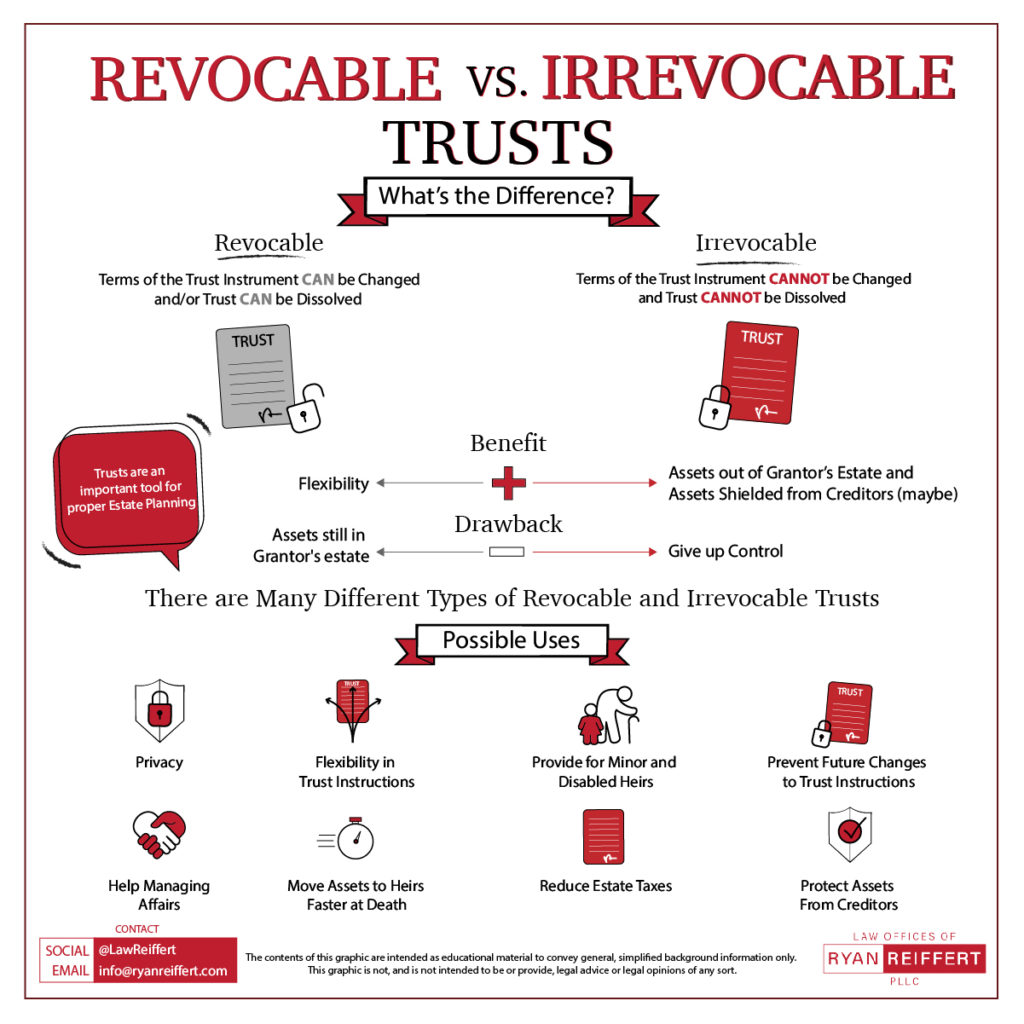

Infographic that explains the difference between a revocable trust vs irrevocable trust

Revocable Trusts

A revocable trust is created by the grantor who also initially serves as the trustee. It can be changed, altered, modified, or revoked at any time during his or her lifetime. Revocable trusts are often (but not exclusively) used as living trusts to avoid probate in the event of the trustor’s death. A revocable trust, because it can be changed, altered, modified, or revoked at will, confers no asset protection benefits during the lifetime of the grantor (a good rule of thumb is that, in order to offer asset protection benefits, some degree of alienation of control must take place). However, upon the death of the grantor, a revocable trust may become an irrevocable trust and serve a different function beyond mere probate avoidance (such change in function is often an integral part of the estate plan).

Living Trusts

A living trust is legally synonymous with a revocable trust, but connotes a slightly different usage. A living trust is a revocable trust that a grantor creates with assets that can still be used throughout his or her lifetime and then transferred to beneficiaries upon their death. While the grantor is alive, he or she may remain the trustee, with a successor trustee or co-trustee. A living trust is generally used for the purpose of probate avoidance and, as with revocable trusts generally, will not confer any asset protection benefits during the lifetime of the grantor.

Irrevocable Trusts

An irrevocable trust is created by the grantor but cannot be changed, altered, modified, or revoked once created. Once assets are placed into an irrevocable trust, they will be managed by the trustee in strict accordance with its terms. No one can take these assets from the trust, including the grantor (although the assets may be exchanged for other assets of equivalent value, in the discretion of the trustee). Unlike a living trust or revocable trust, an irrevocable trust generally affords significant liability protection and shelter from creditors, judgments, etc.

Testamentary Trusts — A testamentary trust, is a type of irrevocable trust created by a will, and the function of which trust supports the instructions of the last will and testament of the trustor.

Why Create a Trust?

There are many reasons people create trusts. A trustor may want to protect assets while also providing a family legacy, ensuring that assets are disbursed in the most beneficial way for their family and heirs. Successful business owners will create trusts to manage their wealth, reduce tax exposure, lessen capital gains, and protect assets from creditors.

Trusts can be used to manage assets, obtain tax reductions or deferrals, and allow for assets to be more easily, cheaply, and quickly disbursed to beneficiaries outside of the probate process.

In addition to being slow, clunky, and expensive, the probate process is also relatively public. An inventory of the estate, as well as various valuations, and the contents of the will itself, are all matters of public record in a probate or heirship proceeding. A trust is not. The transfer of ownership by trust is significantly more private, no public-record court filings are required, no inventory is required, the trust instrument is not publicly filed, and more.

Depending on the type of trust, it may provide an excellent vehicle for management and conservation of assets for future generations, the ability to provide for loved ones who are financially irresponsible or cannot be financially accountable, a way to achieve long-term goals that cannot necessarily be achieved with a will, simply a way to solve some of the deficiencies of the probate process (such as its slow speed, high expense, or public nature), a powerful business planning tool, or even a way for the grantor to better manage, protect, and conserve assets during his or her lifetime.

Above, we outlined four of the basic, and most common types of trusts (the four that you would probably be most likely to have heard of before). Some other types of trusts that we can draft include:

Qualified Domestic Trust (QDOT)

A qualified domestic trust (often abbreviated as “QDOT”) protects marital property from taxes when the surviving partner is not a citizen of the United States.

Normally, and without a QDOT, only a surviving spouse who is a US citizen is eligible for the 100% marital deduction (a non-citizen surviving spouse will be ineligible). This means that all assets will pass from the deceased spouse to the surviving spouse with no limit and no taxes assessed. If the marital deduction does not apply (i.e. the surviving spouse is a noncitizen) then the transfer may be taxable.

Use of a QDOT allows the non-citizen surviving spouse to take advantage of the marital deduction on estate taxes that is usually only allowed for citizens. It can also offer the non-citizen spouse access to any income from the trust’s assets and distributions from any principal in the case of a hardship.

You can think of the QDOT as a “safety net” or “backstop” for a noncitizen spouse.

Marital Deduction Trust

A marital deduction trust is when the trustor places assets in a trust to keep it free from federal transfer taxes upon his or her death. Upon the death of the surviving spouse, the property belongs to the trust and is not included in his or her estate.

Irrevocable Life Insurance Trust (ILIT)

An irrevocable life insurance trust (often abbreviated as “ILIT”) is a type of irrevocable trust that can be a useful estate planning tool for high net worth individuals. Functionally, the ILIT will hold the life insurance policy and usually collect the death benefit as well. This arrangement confers a number of benefits, from reducing the size of the taxable estate, to subsequent asset protection, to leveraging the GST exemption – all while nonetheless conferring some benefits of the proceeds on the beneficiary(ies).

The ILIT will tend to reduce the size of the taxable estate for a few reasons. First, while life insurance payouts are typically excluded from the estate, if the beneficiary is the surviving spouse, the assets would then later be included in that spouse’s estate. Second, appreciation on life insurance policies apart from the death benefit will generally be taxable. By using a properly drafted, structured, and maintained ILIT, both of these non-exempt features can typically be removed from the taxable estate.

Additionally, because the ILIT is an irrevocable trust, it confers the full suite of liability-protection benefits generally attributable to irrevocable trusts, as discussed above. Accordingly, the ability of creditors and litigants to reach the death benefit (and interest) of the life insurance policy can be mitigated.

Finally, the use of an ILIT in conjunction with the GST tax exemption can be extremely powerful. If a grantor allocates his or her GST tax exemption to an ILIT, the value of the life insurance policy in that ILIT over time can (and generally will) increase substantially, resulting a tax-free benefit to multiple generations that will likely end up being much larger than the initially-allocated GST tax exemption.

Crummey Trust(s)

A Crummey trust allows individuals to place the money given pursuant to the annual gift exemption into a restrictive trust (typically in the case of parents giving to children). For most cases other than the use of a Crummey trust, in order to take advantage of the annual gift exemption, the gift must be unrestricted.

However, by allowing a period of unrestricted withdrawal/access to the funds (often 30-60 days) before the funds become restricted and unable to be withdrawn, the parents can “have their cake and eat it, too” by using the (unrestricted) yearly gift exemption to put funds into the (restrictive) trust.

The Crummey trust is named after the pioneer of this technique, Clifford Crummey. The IRS attempted to deny him the annual gift tax exemption based upon the argument that his use of a trust with the features described above failed to meet the “immediate interest” requirement (since it was only subject to withdrawal for a short period of time, and thereafter became inaccessible). The IRS claimed that his contributions to the trust should all count against (reduce) his lifetime gift tax exemption amount.

Mr. Crummey fought the IRS on this, and the courts agreed with him.

Some Variations of the Crummey Trust

A Crummey life insurance trust is an irrevocable gift trust that allows the trustor to exclude life insurance death benefits from his or her taxable estate, reducing or eliminating estate taxes. This is generally used by a trustor with a large taxable estate who is looking for ways to reduce tax burden. The trust is specifically designed to pass assets to the beneficiaries in a way that they will not have to pay gift or estate taxes on the proceeds of the life insurance policy.

A perpetuity Crummey trust combines the above with additional elements of a perpetuity or dynasty trust.

A cross Crummey trust creates trusts for both spouses that enable each to receive lifetime income from the other’s trust.

Elder Trust

An elder trust is often used for an aging individual or for an aging loved one. This trust enables the individual autonomy while still in control of their faculties and capabilities while ensuring that their assets are protected from mismanagement or outside influences.

Perpetuity Trust

A perpetuity trust, perpetual trust, or dynasty trust, is one that, in theory, lasts “in perpetuity” and controls assets for future generations as long as the trustor’s descendants don’t die out. Perpetuity trusts, depending on how they are drafted, allow assets to avoid estate taxes and afford protection from creditors and even the wastefulness of its beneficiaries.

Laws against perpetuity trusts, called “the rule against perpetuities,” have been on the books for many years. Each jurisdiction has its own take on perpetuity trusts and has modified its laws accordingly.

A qualified terminable interest property trust (or “QTIP”) is a trust that gives the grantor the ability to direct how the trust assets will be used to provide for the surviving spouse. Generally either the income or some mix of the income and the principal will be distributed periodically to the surviving spouse for the remainder of the surviving spouse’s life to ensure that the surviving spouse’s needs are met.

A QTIP trust may be used when beneficiaries from a previous marriage exist, and the grantor wishes to care for the surviving spouse as well as provide for those beneficiaries.

A QTIP may also be used to alienate control of the principal amount from the surviving spouse in a situation when a grantor fears that a surviving spouse may be susceptible to influence or pressure from other beneficiaries to access the principal.

Finally, because a QTIP is a species of irrevocable trust, it therefore offers similar creditor/judgment protection to the other irrevocable trusts.

Credit Shelter Trust

A credit shelter trust is one where the trustor has placed assets into the trust to benefit younger beneficiaries who may be too young to manage the assets upon the trustor’s death. If there is a surviving spouse, he or she can still benefit from assets under conditions set out in the trust.

Some credit shelter trusts are created to control particular assets with special provisions. Some provisions provide for vacation homes if the grantor wants to ensure that the home is retained for future generations or include firearm provisions that entitle the trust to own firearms without NFA registry.

Two-Party Credit Shelter Trust

A two-party credit shelter trust is another form of credit shelter trust that will have the same provisions but for a couple who is not married. This trust can provide for the surviving partner upon the death of the trustor and their children or other beneficiaries upon both parties’ death.

Qualified Subchapter S Trust

The shareholders of a Subchapter S corporation must pay income tax on the corporate earnings. For a trust to be considered a shareholder, it must pass on the Subchapter S corporation’s income, through a qualified subchapter S trust, to a beneficiary who will then declare the income. That beneficiary must be a U.S. citizen. (the requirements of a Subchapter S trust are very similar to the requirements of the S-Corporation!)

Generation Skipping Trusts

The IRS levies a “generation skipping transfer tax” – or GST tax – on gifts from grandparents to grandchildren (skipping the parents).

The goal of this tax scheme is to ensure that taxes are paid at each generational level and that rich families cannot effectively reduce their tax rate by half simply by playing “leapfrog” between generations.

Accordingly, if the GST tax is triggered and the exemption has been used, the taxes imposed can be roughly doubled.

A generation skipping trust (or GST-exempt trust) is where assets are specifically passed down to the trustor’s grandchildren or anyone who is at least 37 ½ years younger than the trustor and is not a spouse or former spouse, thereby “skipping” the trustor’s children (such person, who need not actually be related, is referred to as a “skip person” in the GST tax context). Bypassing the trustor’s children can potentially avoid one round of the double-round estate taxes that would normally be imposed if the grandchildren were direct beneficiaries.

The proper formulation and use of a GST-exempt trust is difficult and complicated, so it is important to contact an attorney, banker, and accountant as soon as possible if you are considering this device as part of your estate plan.

Educational Trusts

Educational trusts are designed to provide for the educational costs of a grantor’s children or grandchildren. This trust ensures that the funds are used only for the purposes intended while maintaining control of the assets. It can also include language allowing for exclusion of the gift tax with a Crummey power to create a present right to a future interest.

Supplemental Needs Trusts or Special Needs Trusts

A supplemental needs trust or special needs trust serves to help meet the needs of family members with disabilities without them losing essential public benefits. A special needs or supplemental needs trust will provide for things such as medical and dental expenses and equipment, education, transportation, essential dietary needs, and many other needs and services that supplement government program provisions.

Income-Only Trust (Medicaid Trust)

An income-only trust (sometimes called a Medicaid Trust since one common use of these trusts is to ensure eligibility for Medicaid) offers a way that a trustor can transfer assets to a trust while still earning income from those assets. These assets are generally income-producing assets such as CDs, stocks, bonds, investment properties, or other income-producing interests. Income-only trusts are generally used for Medicaid eligibility while still preserving other assets for use by the trustee.

Charitable Remainder Trusts

A charitable remainder trust is a tax-exempt irrevocable trust that is designed to provide income to the beneficiaries until death or for a finite period of time. The trustor can be named as a beneficiary and get a charitable tax deduction for the year that the trust is funded. Upon death or at the end of the designated time period, the remainder of the trust goes to charity. There are two types of charitable remainder trusts:

A charitable remainder unitrust (CRUT) is funded by real estate or other valuable assets and can be added to over time. It will distribute a percentage of the value of the assets as they are revalued on an annual basis, with the remainder going to charity. The donated amount must be at least 10 percent of the asset’s value.

A charitable remainder annuity trust (CRAT) is funded by assets which will pay a fixed annuity at regular intervals instead of a percentage of the value.

Charitable Lead Trusts

Whereas a charitable remainder trust makes distributions to beneficiaries with the remainder going to charity, a charitable lead trust makes distributions to the charity for a finite period of time. After that time, the balance is then paid to the beneficiary. This trust provides tax deductions for charitable donations as well as protections against estate and gift taxes.

Qualified Personal Residence Trusts

A qualified personal residence trust is an irrevocable trust that allows a trustor to remove the value of a personal residence from his or her taxable estate. This trust will allow the trustor to remain in the home for a period of time as retained interest. Once that time period is over, the property is then owned by the remainder beneficiaries based on the property’s appraised value when it was placed into the trust, reducing estate taxes.

Grantor Retained Income Trusts

A grantor retained income trust is an irrevocable trust that is fixed for a finite period of time. It allows the trustor to retain income from the assets in the trust or use of a property in the trust during its existence. At the end of the time period, the remaining principal goes on to the beneficiaries.

Grantor Retained Annuity Trust

A grantor retained annuity trust is an irrevocable trust that is fixed. After the grantor funds the trust, he or she will receive annuity payouts from it. After the annuity period ends, the remaining value of the trust gets disbursed to the beneficiaries.

Grantor Retained Unitrust

A grantor retained unitrust is similar to a grantor retained annuity trust but different in how payouts are made to the grantor. Payouts are based on a fixed percentage of the trust’s value. Consequently, as the value of the trust changes over the course of the term of the trust, payouts can change. At the termination of the trust, the remaining value of the trust gets disbursed to the beneficiaries.

Incentive Trusts

An incentive trust is one set up by a trustor to provide support during his or her lifetime and then pass on the assets to the beneficiary(s) with conditional provisions. This type of trust is typically used when a trustor wants to ensure that the beneficiary(s) behavior or self-sufficiency warrants the disbursement of the funds. The trustee must make judgments regarding whether the beneficiary has met those requirements.

Asset Protection Trusts

An asset protection trust is an irrevocable self-settled trust where the grantor is also the beneficiary (but the trustee will be another party). The trust’s primary goal is to protect assets from potential creditors. If a creditor were to obtain a judgment against the maker, that creditor will only have the ability to “take” the annual distributions made to the maker. The creditor will be prevented from proceeding against the principal of the trust, as it is not under the maker’s control.

Along with other strategies of exempting and shielding other assets, this strategy can provide significant leverage against a creditor, as well as a way to protect one’s assets against unscrupulous plaintiffs or plaintiff attorneys.

While the asset protection trust can be associated or combined with some of the other trusts described on this page, it is not necessary to do so.

Delaware Asset Protection Trust

Delaware is one of the most advantageous states in which to set up an asset protection trust (very similar to the way in which Delaware is a common place for corporations and LLCs to form, due to its favorable business law provisions).

A Delaware asset protection trust is simple an asset protection trust that is located in Delaware. It can confer some marginal benefits over other state trusts, depending upon the state. Consult your attorney and tax advisor for more information.

Offshore Trusts

Offshore asset protection can involve the formation of a trust in a favorable jurisdiction outside the country. An offshore trust is one that is created and holds assets outside of the United States to protect them. In an offshore trust, both assets and the trustee are outside the legal jurisdiction of the United States and courts and creditors have no legal means to interfere with or take action with these assets.

Traditionally, Switzerland had some of the strongest bank secrecy laws in the world. However, that is no longer the case. Another of the most common choices for an offshore trust is the Cook Islands, whose government has frequently resisted the United States government’s attempts to seize assets located there. Another common choice for an offshore trust may be a country where the grantor and/or beneficiary holds dual citizenship and/or has other family ties.

Blind Trusts

A blind trust is one that is set up by a trustor, giving the trustee full management of and income generated by the assets without the beneficiary(s) knowledge. These can be established to avoid conflicts of interest, conflicts between trustees and beneficiaries, or conflict between beneficiaries.

Blind trusts are very commonly used by political figures in the United States in order to avoid bias or the appearance of bias when advocating policy positions.

Pet Trusts

Under Texas law, a pet is considered to be personal property, and has no independent legal rights. While this may be bizarre and incorrect in the view of many pet owners, who view their dog or cat as closer to a son, daughter, or friend, than a chair or lamp, it is nonetheless settled law in the state of Texas.

A pet trust allows a grantor to sort of “get around” this legal problem by setting aside funds for the care of a pet after the grantor’s death (or, potentially, in case of the grantor’s disability) until the natural death of the animal.

Reasons to work with us

Why Choose Ryan As Your Business Attorney

01

Excellent Track Record

If you are a startup navigating legal waters for the first time or a small business…

If you are an established business looking for a high-quality corporate lawyer…

If you are an individual seeking to protect yourself…

If this is “not your first rodeo” and you don’t need hand-holding, you just need a seasoned

deal-closer…

If your family business is looking for guidance on how to expand or break new ground…

02

Fee Transparency

Legal work can be expensive, and nobody likes a surprise bill.

Having been in-house General Counsel, I have been in that boat, too.

I can’t cover all your legal needs for free, but I can help you think about which expenses make

sense and which expenses don’t… before we start the clock.

Unlike some of the larger and older law firms, I can also help with some unique and tailored

alternative fee arrangements.

03

Personal Attention

My philosophy is simple. I believe that when you hire an attorney, that attorney should handle

your issue.

Therefore, when you hire me, I will handle your issue.

When you call my office, you will talk to me (unless I am meeting with another client).

When you have questions, I will be the one answering them (if I can).

Contact Us

The attorney responsible for this site for compliance purposes is Ryan G. Reiffert.

Unless otherwise indicated, lawyers listed on this website are not certified by the Texas Board of Legal

Specialization.