Tax planning involves the analysis of the financial and legal affairs of a person or family, and the efficient structuring or arranging of those affairs in such a way as to maximize the impact of tax breaks, credits, incentives, etc. and minimize (and/or defer) tax liabilities.

Of course, this is much easier said than done.

At the outset, it should be noted that this is not a SOLELY legal issue. A tax planning strategy is one that should be discussed seamlessly with your lawyer, your accountant, your banker, and others. This is one of the strengths Law Offices of Ryan Reiffert brings to the table – long-term relationships with other professionals in the field.

For an individual, couple or business whose income is highly variable (specifically, one that puts them in a different tax bracket from year to year), the timing of realizing certain gains or losses should, if it at all possible, be deliberate. The following table, which shows the tax brackets for the year 2020, illustrates why this is the case:

Tax Planning Examples

Single*

Tax rate

Taxable income bracket

Tax owed

10%

$0 to $9,875

10% of taxable income

12%

$9,876 to $40,125

$987.50 plus 12% of the amount over $9,875

22%

$40,126 to $85,525

$4,617.50 plus 22% of the amount over $40,125

24%

$85,526 to $163,300

$14,605.50 plus 24% of the amount over $85,525

32%

$163,301 to $207,350

$33,271.50 plus 32% of the amount over $163,300

35%

$207,351 to $518,400

$47,367.50 plus 35% of the amount over $207,350

37%

$518,401 or more

$156,235 plus 37% of the amount over $518,400

Married Filing Jointly*

Tax rate

Taxable income bracket

Tax owed

10%

$0 to $19,750

10% of taxable income

12%

$19,751 to $80,250

$1,975 plus 12% of the amount over $19,750

22%

$80,251 to $171,050

$9,235 plus 22% of the amount over $80,250

24%

$171,051 to $326,600

$29,211 plus 24% of the amount over $171,050

32%

$326,601 to $414,700

$66,543 plus 32% of the amount over $326,600

35%

$414,701 to $622,050

$94,735 plus 35% of the amount over $414,700

37%

$622,051 or more

$167,307.50 plus 37% of the amount over $622,050

Married Filing Separately*

Tax rate

Taxable income bracket

Tax owed

10%

$0 to $9,875

10% of taxable income

12%

$9,876 to $40,125

$987.50 plus 12% of the amount over $9,875

22%

$40,126 to $85,525

$4,617.50 plus 22% of the amount over $40,125

24%

$85,526 to $163,300

$14,605.50 plus 24% of the amount over $85,525

32%

$163,301 to $207,350

$33,271.50 plus 32% of the amount over $163,300

35%

$207,351 to $311,025

$47,367.50 plus 35% of the amount over $207,350

37%

$311,026 or more

$83,653.75 plus 37% of the amount over $311,025

Head of Household*

Tax rate

Taxable income bracket

Tax owed

10%

$0 to $14,100

10% of taxable income

12%

$14,101 to $53,700

$1,410 plus 12% of the amount over $14,100

22%

$53,701 to $85,500

$6,162 plus 22% of the amount over $53,700

24%

$85,501 to $163,300

$13,158 plus 24% of the amount over $85,500

32%

$163,301 to $207,350

$31,830 plus 32% of the amount over $163,300

35%

$207,351 to $518,400

$45,926 plus 35% of the amount over $207,350

37%

$518,401 or more

$154,793.50 plus 37% of the amount over $518,400

* again, these rates are for the 2020; the charts for 2021 will look a little different

If you find yourself close to one of these cutoffs, whatever your tax rate and income level is, you could be throwing away real money by timing your gains and losses incorrectly.

Here is a very, very simple and very, very contrived example of why timing matters. Let’s suppose a single person who received an unusually large bonus at work this year, that pushed his or her income to $163,299 (one dollar below the cutoff for the jump from the 24% to 32% marginal tax bracket). But next year, he or she anticipates an income that is around $110,000 (an income level solidly in the middle of the 24% tax bracket). This person is considering, on December 30th, whether to sell $10,000 worth of stock (held for less than a year). If they he or she were to sell in December, the tax on that $10,000 will be taxed at the full 32% due to the other income already generated during that time (the stock would not qualify for preferential long-term capital gains treatment since it was held for less than a year), so the tax will be $3,200, leaving the unlucky taxpayer with $6,800. However, if he or she were to wait a few days and sell on in January 1st instead, the tax would be 24%, or $2,400, leaving our taxpayer with $7,600. That’s a quick $800 just for waiting two days to sell.

Of course, further to the example above, there is always a risk to waiting to sell stock (the price may go down) or to delaying any other business transaction. Evaluating, balancing, and (if possible) mitigating this risk is part of the value that a competent team of advisors, including an attorney and an accountant, bring to the table.

This concept could apply to business transactions as well, but often those transactions have more factors and are more complex. It may be as simple as waiting a few days to sell stock. There may be other parties involved or other hurdles.

This is a very simplistic example, dealing with a relatively small amount, but once you start dealing with other types of taxes and adding zeroes, the benefits of proper planning become much more powerful.

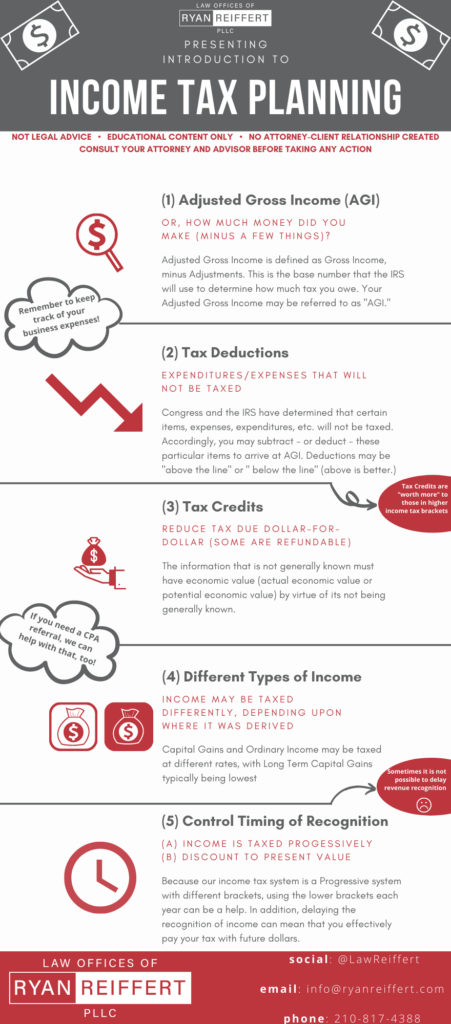

Additionally, understanding the difference between a tax credit and a tax deduction is important here. A tax credit reduces tax due, whereas a tax deduction reduces the income on which tax is payable. Therefore, tax credits are worth the same amount of dollars to everyone, but tax deductions are more valuable to those in higher income brackets.

For example, a $1,000 income tax credit is worth $1,000 to someone in the 10% bracket; it’s worth $1,000 to someone in the 24% bracket; and it’s worth $1,000 to someone in the 37% bracket. Conversely, a $1,000 income tax deduction is worth $100 to someone in the 10% bracket, but is worth over twice as much ($240) to someone in the 24% bracket, and almost four times as much ($370) to someone in the 37% bracket. So, tax credits and tax deductions are both fantastic, but credits equally fantastic for everyone; deductions, on the other hand, are more fantastic if you’re a high income person in a high tax bracket.

If you’re following all of this, you see the need for quality tax planning advisors. If you’re not following, it’s OK.

Other tax planning strategies could potentially include above-the-line deductions vs. below-the-line deductions, the timing of charitable deductions, or in some cases forming one’s own charitable foundation, and much much more.

It also involves the strategic timing of realizing certain deductions or gains. It might be beneficial to realize a gain (or loss) in December of this year vs. January of next year, depending upon what the rest of the tax picture looks like. Running parallel to this set of concerns is the time value of money in general – would you rather lose a dollar now, three months from now, or a year from now? Most people would prefer to defer that loss for as long as possible.

And this is where proper tax planning comes into the equation.

Another important realization in this context is that different types of income are sometimes taxed differently. Dividends and long-term capital gains (currently) receive vastly preferential tax treatment to ordinary income or short-term capital gains. This difference in the taxation of different types of income is part of what accounts for Warren Buffett’s observation that he pays roughly the same tax rate as his secretary.

Tax Planning FAQs

Q: So you’re going to tell me how to pay no taxes? That’s awesome! I hate paying taxes!

A: No. Generally speaking, your tax bill will not be $0 unless your income is $0 (or close to $0). Tax dodging or tax evasion is illegal, and is a really great way to end up in prison. Keep in mind that if someone is selling you something that seems “too good to be true”, it probably is.

Q: OK, so I have to pay something, but you’ll help me pay less?

A: Something like that. I can help you reduce your tax bill through legal means. That’s why we call it “tax planning” and not “tax evasion”.

Q: But what about all the TAX LOOPHOLES that I always hear about? Surely you can help me find some loopholes, right?

A: There was a lot of that a few decades ago (some of which landed people with fines or jail sentences, and some of which they got away with). But it’s mostly gone now, at least for individuals. Some large multinational corporations continue to use a scheme known as “Double Irish with a Dutch Sandwich” to defer their taxes, but that isn’t an option for most individuals.

Q: OK, fine. But what about a Swiss bank account? They’re all about bank secrecy! They don’t tell anybody anything!

A: Hollywood loves this trope, but it’s not really accurate, at least not any more. Legality of this strategy aside, there may have been some truth to it decades ago, but nowadays, not so much.

Tax Planning Services offered by Ryan Reiffert

So where does all of this leave us?

Two of the obvious first steps to take, if you’re looking to minimize taxes overall and efficiently structure payment are (1) call your attorney and (2) call your accountant.

Reasons to work with us

Why Choose Ryan As Your Business Attorney

01

Excellent Track Record

If you are a startup navigating legal waters for the first time or a small business…

If you are an established business looking for a high-quality corporate lawyer…

If you are an individual seeking to protect yourself…

If this is “not your first rodeo” and you don’t need hand-holding, you just need a seasoned

deal-closer…

If your family business is looking for guidance on how to expand or break new ground…

02

Fee Transparency

Legal work can be expensive, and nobody likes a surprise bill.

Having been in-house General Counsel, I have been in that boat, too.

I can’t cover all your legal needs for free, but I can help you think about which expenses make

sense and which expenses don’t… before we start the clock.

Unlike some of the larger and older law firms, I can also help with some unique and tailored

alternative fee arrangements.

03

Personal Attention

My philosophy is simple. I believe that when you hire an attorney, that attorney should handle

your issue.

Therefore, when you hire me, I will handle your issue.

When you call my office, you will talk to me (unless I am meeting with another client).

When you have questions, I will be the one answering them (if I can).

Contact Us

The attorney responsible for this site for compliance purposes is Ryan G. Reiffert.

Unless otherwise indicated, lawyers listed on this website are not certified by the Texas Board of Legal

Specialization.

So where does all of this leave us?

Two of the obvious first steps to take, if you’re looking to minimize taxes overall and efficiently structure payment are (1) call your attorney and (2) call your accountant.

So where does all of this leave us?

Two of the obvious first steps to take, if you’re looking to minimize taxes overall and efficiently structure payment are (1) call your attorney and (2) call your accountant. So where does all of this leave us?

Two of the obvious first steps to take, if you’re looking to minimize taxes overall and efficiently structure payment are (1) call your attorney and (2) call your accountant.

So where does all of this leave us?

Two of the obvious first steps to take, if you’re looking to minimize taxes overall and efficiently structure payment are (1) call your attorney and (2) call your accountant.