What You Should Know Before You Sign a Commercial Lease

As a new or even experienced business owner, signing the lease on a commercial space can be a complicated venture and, depending on availability, can demand some patience and a lot of homework. In the business world, knowledge is power. Unfortunately, lack of knowledge can trip you up and cause untold stress and financial and legal heartache. Before you venture into the world of leasing commercial property and signing a commercial lease, arm yourself with information.

Research is your new best friend as you try to understand the type of property you need, the size, and all the other incidentals that go into leasing a commercial space. One of the best ways to do that is to speak with an experienced San Antonio business lawyer or a commercial real estate attorney who you can trust.

Understand Your Needs

Like anything else, it’s better to understand your needs before you seek out prospects. Looking at commercial property will be overwhelming without understanding exactly what you are looking for, the geographic area you want to target, and how much you can afford to pay.

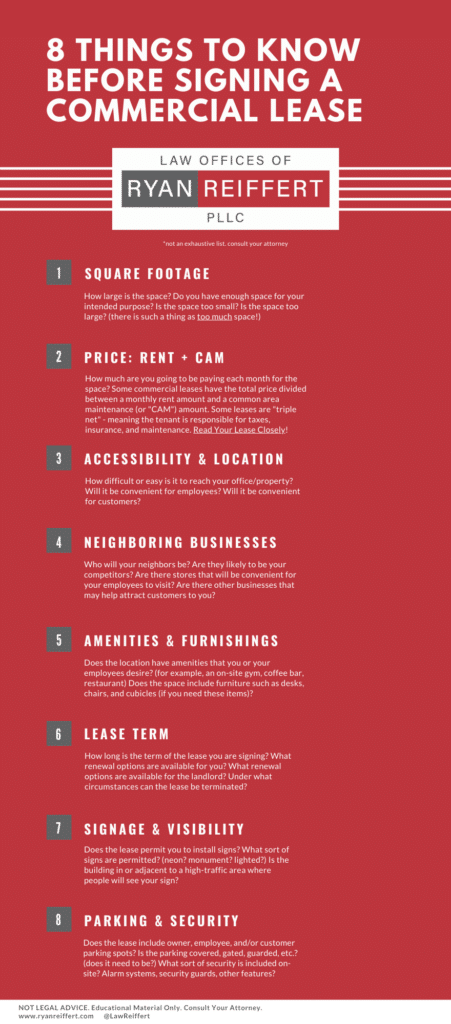

Consider your space. Some spaces will require modifications such as provisions for offices or cubicles within the larger area, or additional wiring for better communications systems.

Consider your competition. Do you have competitors in the area? Will the landlord be able to lease to a competitor once you are in? You should understand the concept of exclusive-use phrasing in your lease as this may be very important to ensuring against competition setting up in the same building.

Who is the building owner? The landlord? The landlord is often not the building owner. Know as much as you can about both. You would never go into a partnership with someone you didn’t know. Your lease is a business partnership. Check the public records, ask other tenants, ask your San Antonio commercial real estate lawyer or a commercial real estate professional. There are many ways a tenant/landlord relationship can go awry. Don’t let that happen to you.

Understand What Kind of Property and Area You Are Looking For

You may have a product with a specific demographic you want to be near, you may want your signage to be seen from the road, you may need industrial space with loading docks, or you may just be looking for a small office. Regardless of what you are looking for, you want to understand and target specific areas based on those needs and understand the different types of commercial properties.

Know the Laws

Regardless of whether the landlord or the broker assures you that you are fine under local zoning or other municipal or state laws, do your own homework. Once you are in, it becomes your headache to fix if you can’t operate legally under the current laws. Nuisance and environmental stipulations and regulations can also trip you up. The landlord or broker may not even be aware of them.

A Commercial Lease is a Different Animal

Although you may be familiar with a residential lease agreement, the similarity to commercial leases is that they are completely different animals. The world of the commercial lease is far more broad, more flexible, more negotiable, but it also offers less protections for you as a tenant. Consider that

Consider your space. Some spaces will require modifications such as provisions for offices or cubicles within the larger area, or additional wiring for better communications systems.

Consider your competition. Do you have competitors in the area? Will the landlord be able to lease to a competitor once you are in? You should understand the concept of exclusive-use phrasing in your lease as this may be very important to ensuring against competition setting up in the same building.

Who is the building owner? The landlord? The landlord is often not the building owner. Know as much as you can about both. You would never go into a partnership with someone you didn’t know. Your lease is a business partnership. Check the public records, ask other tenants, ask your San Antonio commercial real estate lawyer or a commercial real estate professional. There are many ways a tenant/landlord relationship can go awry. Don’t let that happen to you.

Understand What Kind of Property and Area You Are Looking For

You may have a product with a specific demographic you want to be near, you may want your signage to be seen from the road, you may need industrial space with loading docks, or you may just be looking for a small office. Regardless of what you are looking for, you want to understand and target specific areas based on those needs and understand the different types of commercial properties.

Know the Laws

Regardless of whether the landlord or the broker assures you that you are fine under local zoning or other municipal or state laws, do your own homework. Once you are in, it becomes your headache to fix if you can’t operate legally under the current laws. Nuisance and environmental stipulations and regulations can also trip you up. The landlord or broker may not even be aware of them.

A Commercial Lease is a Different Animal

Although you may be familiar with a residential lease agreement, the similarity to commercial leases is that they are completely different animals. The world of the commercial lease is far more broad, more flexible, more negotiable, but it also offers less protections for you as a tenant. Consider that

Consider your space. Some spaces will require modifications such as provisions for offices or cubicles within the larger area, or additional wiring for better communications systems.

Consider your competition. Do you have competitors in the area? Will the landlord be able to lease to a competitor once you are in? You should understand the concept of exclusive-use phrasing in your lease as this may be very important to ensuring against competition setting up in the same building.

Who is the building owner? The landlord? The landlord is often not the building owner. Know as much as you can about both. You would never go into a partnership with someone you didn’t know. Your lease is a business partnership. Check the public records, ask other tenants, ask your San Antonio commercial real estate lawyer or a commercial real estate professional. There are many ways a tenant/landlord relationship can go awry. Don’t let that happen to you.

Understand What Kind of Property and Area You Are Looking For

You may have a product with a specific demographic you want to be near, you may want your signage to be seen from the road, you may need industrial space with loading docks, or you may just be looking for a small office. Regardless of what you are looking for, you want to understand and target specific areas based on those needs and understand the different types of commercial properties.

Know the Laws

Regardless of whether the landlord or the broker assures you that you are fine under local zoning or other municipal or state laws, do your own homework. Once you are in, it becomes your headache to fix if you can’t operate legally under the current laws. Nuisance and environmental stipulations and regulations can also trip you up. The landlord or broker may not even be aware of them.

A Commercial Lease is a Different Animal

Although you may be familiar with a residential lease agreement, the similarity to commercial leases is that they are completely different animals. The world of the commercial lease is far more broad, more flexible, more negotiable, but it also offers less protections for you as a tenant. Consider that

Consider your space. Some spaces will require modifications such as provisions for offices or cubicles within the larger area, or additional wiring for better communications systems.

Consider your competition. Do you have competitors in the area? Will the landlord be able to lease to a competitor once you are in? You should understand the concept of exclusive-use phrasing in your lease as this may be very important to ensuring against competition setting up in the same building.

Who is the building owner? The landlord? The landlord is often not the building owner. Know as much as you can about both. You would never go into a partnership with someone you didn’t know. Your lease is a business partnership. Check the public records, ask other tenants, ask your San Antonio commercial real estate lawyer or a commercial real estate professional. There are many ways a tenant/landlord relationship can go awry. Don’t let that happen to you.

Understand What Kind of Property and Area You Are Looking For

You may have a product with a specific demographic you want to be near, you may want your signage to be seen from the road, you may need industrial space with loading docks, or you may just be looking for a small office. Regardless of what you are looking for, you want to understand and target specific areas based on those needs and understand the different types of commercial properties.

Know the Laws

Regardless of whether the landlord or the broker assures you that you are fine under local zoning or other municipal or state laws, do your own homework. Once you are in, it becomes your headache to fix if you can’t operate legally under the current laws. Nuisance and environmental stipulations and regulations can also trip you up. The landlord or broker may not even be aware of them.

A Commercial Lease is a Different Animal

Although you may be familiar with a residential lease agreement, the similarity to commercial leases is that they are completely different animals. The world of the commercial lease is far more broad, more flexible, more negotiable, but it also offers less protections for you as a tenant. Consider that

- A commercial lease is typically for a longer term, usually from 3 to 5 years, is a legally binding contract between your business and the landlord, and is not easily broken. Because there is usually a good bit of money at stake, it is essential that you understand your terms before you sign on the dotted line.

- A commercial lease offers less in the way of consumer protections. Commercial leases aren’t subject to the same protections as residential leases.

- A commercial lease agreement is fully customized, not using a standardized format, and usually to the benefit of the landlord. Make sure you have read it and understand it completely.

- The good news! A commercial lease is far more flexible and negotiable. Depending on the market in your area and how eager the landlord is to lease the space, you may be able to work in some features to your advantage.

- Base rent — Base rent calculated on an amount per usable square foot

- Usable square feet — Amount of square footage that is reserved for a tenant, not including shared spaces

- Rent increase — Rental amount that can change from year to year typically based on a percentage of the rent. This can often be negotiated or capped.

- Lease deposit — Monetary sum that holds space until the agreement is finalized. This is typically a security deposit plus two months rent.

- Security deposit — Money held in advance against damages and to secure performance under the lease.

- Length of lease — Indicates start and end dates of the lease term, typically from 3 to 5 years in duration

- Improvements — Indicates the types of improvements or upgrades that can be made to the space. It will also set out who is responsible for the costs of these. These are typically negotiable.

- Grant of lease — Clause that stipulates that the landlord will turn over the property upon all conditions being met

- Commencement date — Date that tenant takes over and becomes responsible for rent and terms

- Extension — Parties may agree to an extension of the agreement in writing

- Late fees — Conditions by which a tenant, if late in paying rent, will be subject to extra fees, which may be a flat fee or percentage of the rent

- Taxes — Outlines all taxes associated with the space and who is responsible for paying them.

- Obligation for repair — Stipulates the types of repairs that the landlord and tenant are obligated to make and who will be responsible for making them

- Permits — Parties will be required to get necessary permitting and licensing for improvements or repairs.

- Covenants — Each party has a separate set of covenants setting out further requirements and responsibilities of each.

- Indemnity by tenant — Removes liability from the landlord in cases of damage, loss, injury, or claims unless they are caused by omissions, willful acts, or gross negligence by the landlord.

- Rent abatement or adjustment — The rent will be eliminated or adjusted in the event of fire or disaster.

- Condemnation — Sets out what will happen if the property is taken by government powers of condemnation or eminent domain.

- Option to purchase — Tenant has the right to purchase the property during the term of the lease for an agreed-upon price. It can also state that the tenant does not have the right of purchase.

- Exterior or interior modifications

- Utilities

- Insurance

- Property taxes

- Exterior and interior maintenance

- Repairs

- Security

- Parking

- How can your lease be transferred if you choose to leave or the business ends up closing? Will you be allowed to assign the lease or sublet to another tenant? In either case, you will typically need to get prior written consent.

- Will you be required to sign a personal guarantee? This means that you will be personally responsible for the lease should the business fail and is a risk you may not choose to take on.

- If you choose or need to stay on past the lease expiration, how will any holdover rent be handled? In many cases, a landlord will add a clause that will make your business responsible for up to 250 percent of the monthly rent should you not be prepared to vacate at the end of the lease. This can and should be negotiated.

- If the landlord or owner fails to pay the mortgage on the property, will you be evicted even though you have paid your monthly payments on time? If you have a nondisturbance agreement, you will be allowed to stay and continue paying your rent to whoever eventually takes over the building.