Business and Estate Planning law firm. Established in February 2020. 125+ 5-star reviews. Offices in San Antonio and San Marcos, Texas.

Share

How Bankruptcy Works: a short overview for businesses and individuals

As a San Antonio business lawyer, I get all kinds of different questions about options available to businesses – from prospering and growing businesses who have questions about M&A, to troubled businesses who want to explore options for restructuring or liquidation like bankruptcy.

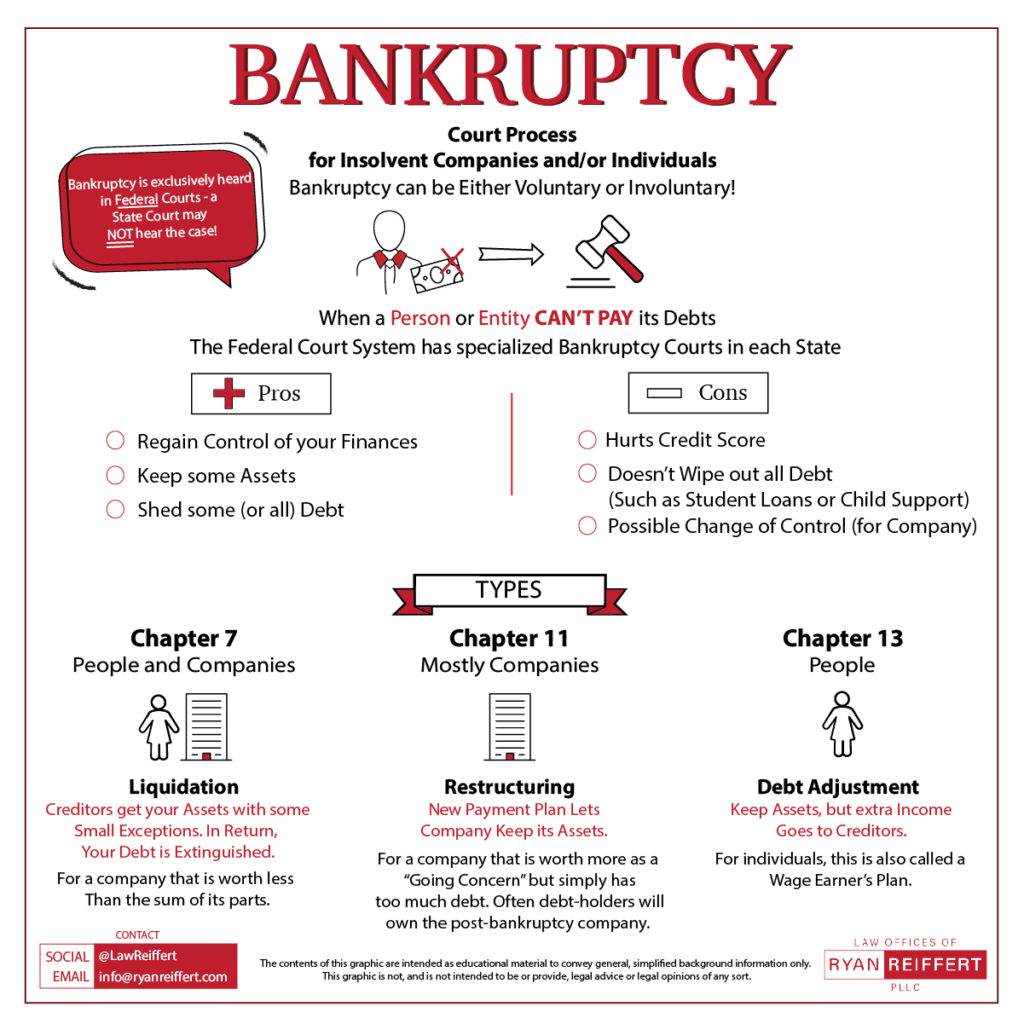

Bankruptcy is based on federal law – the United States Bankruptcy Code – and there are federal courts exclusively devoted to hearing bankruptcy cases – the United States Bankruptcy Courts.

Fundamentally, the bankruptcy process is intended to help financially troubled individuals and businesses to discard some or all of their debts or make a court-approved plan to repay those debts.

Three Main Types of Bankruptcy

There are, mainly, three different types of bankruptcy, designed for three different financial situations. One of these can apply to both businesses and individuals, another is primarily for businesses, and the third is primarily for individuals. These three types of bankruptcy are generally referred to according to the chapter of the U.S. Bankruptcy Code that establishes and governs that type of bankruptcy.

bankruptcy infographic

Chapter 7 Bankruptcy (Liquidation)

In a Chapter 7 bankruptcy, also known as a liquidation, all (or almost all) of the debtor’s debts are extinguished, and all (or almost all) of the debtor’s assets are distributed to the creditors.

For an individual, a Chapter 7 Bankruptcy is essentially a case where the debtor gives all of its assets to its creditors, in exchange for al current debts. It can be thought of as something like “the nuclear option” when a Chapter 13 (discussed below) is not available or practical. Some individuals have gotten in big trouble during a Chapter 7 for attempting to hide assets or engage in fraudulent transfers of assets, ahead of the bankruptcy.

For a business, a Chapter 7 is for a business that has, essentially, failed. The assets of the business will be sold, and the proceeds will be distributed to the creditors, in order of seniority by class of debt and proportionally within each class. A Chapter 7 bankruptcy is for the business that is worth less as a going concern than the sum of its parts. As a result of the Chapter 7, all the assets of the company would be sold, and the company would be terminated.

Chapter 11 Bankruptcy (Restructuring)

Chapter 11 is mainly for companies, not individuals. It is also known as a restructuring, because the debts of the company will be restructured, but the company will not be terminated or dissolved.

A Chapter 11 bankruptcy will be appropriate in the situation where the business does make money, but simply cannot service its debt. In contrast to the Chapter 7 bankruptcy (liquidation), where the business is worth less as a going concern than the sum of its parts, in a Chapter 11 (restructuring), the business is worth more as a going concern than the sum of its parts.

Depending upon the exact structure of the debts, some junior debt of the company may be extinguished. Other debts may stay in place. Perhaps senior debtholders will be paid off, or will remain as debt of the surviving company. There may be a “fulcrum class” of debt that will become the new equity or stockholders of the company.

Chapter 13 (Wage Earner’s Plan)

A Chapter 13 bankruptcy is mainly for individuals with a regular income. This chapter allows individuals who have a regular income to “split off” part of that income to pay creditors and eventually pay down their debts. Chapter 13 is also often called a “Wage Earner Plan.”

Generally these installment payments to creditors are structured to be made under a three-year to five-year plan.

Some Other Types of Bankruptcy

There are other, less common, types of bankruptcy protection that you may apply for under the Bankruptcy Code.

Chapter 9 Bankruptcy: available to municipalities (such as cities, towns, and subdivisions of those cities and towns such as taxing districts, municipal utilities, and school districts, etc.) that wish to reorganize.

Chapter 12 Bankruptcy: available to family farmers and fishermen that desire debt relief

Chapter 15 Bankruptcy: applicable to filings that involve parties from more than one country

Voluntary vs Involuntary Bankruptcy

Frequently, a bankruptcy case will be initiated by a debtor who files a petition with a U.S. Bankruptcy Court. The petition can be filed by an individual, jointly by spouses, or by a company.

On other occasions, a person or business may be forced into bankruptcy by creditors, through the filing of an involuntary bankruptcy petition. An involuntary bankruptcy petition can only be made under Chapter 7 or Chapter 11.

A great example of a case for an involuntary bankruptcy is the situation where the debtor has the ability to pay its debts, but not the willingness to do so. Alternatively, an involuntary bankruptcy might also be appropriate for a debtor who is headed toward bankruptcy but is paying its debts in an uneven or unfair way, and the creditors wish to charge that these uneven payments constitute fraudulent transfers and invoke the power of the court.

The filing of an involuntary bankruptcy petition is relatively rare – but it does happen from time to time.

More Information

While bankruptcy representation is not presently one of the services that we offer at Law Offices of Ryan Reiffert, PLLC, we hope that this introduction has been helpful to you. If you do have a bankruptcy matter, we are more than happy to make a referral to a qualified colleague. Contact us for more information.

){kind=link}