S-Corporation: Tax Reduction and Liability Protection for Small Business

You may have heard of S-Corporations before. Odds are good that if you have heard of the S-Corporation, it was in the context of a tax reduction strategy. The S-Corporation is one of the great intersections of business entity liability protection, asset protection, and tax reduction.

Which is one of the things they’re good for. But they’re also good for much more than that, as I discuss in this brief summary video from my YouTube channel.

(PLEASE CONSIDER SUBSCRIBING FOR LEGAL NEWS AND EXPLANATIONS!)

As I note in the video above, there is actually no such entity as an “S-Corporation”… the thing that people refer to as an “S-Corporation” is, from a legal perspective, just a regular corporation. Like any other corporation, from your neighbor’s car washing business to the biggest behemoths of the Fortune 500. The “S” in “S-Corporation” actually is a tax distinction, not a legal distinction. An S-Corporation is a corporation that has validly filed with the IRS a Form 2553 Election by a Small Business Corporation, the effect of which is to pass all taxable effects from the entity through to the shareholders in proportion to their ownership of the corporation – including income, loss, credits, deductions, realized gains, etc. All of it.

In contrast, a corporation that has not made the S-Election is called a C-Corporation (legally indistinguishable – just a corporation) because it is taxed under subchapter C rather than subchapter S. In practical terms, that means that the earnings of a C-Corporation are taxed twice – first the corporation itself pays taxes on its earnings at the corporate level; and taxed again as dividends, if and when such earnings are distributed to the shareholders.

In almost all circumstances, being taxed as a C-Corporation is a very bad deal – something to be assiduously avoided if at all possible.

In many cases, avoiding C-Corporation taxation actually is possible – via the S-Election, as filed on Form 2553.

Here are some* of the benefits of using the S-Corporation for your business:

Limited Liability & Asset Protection: Just like many other business entities (such as Limited Liability Companies (LLCs), C-Corps, Limited Partnerships (LPs), Limited Liability Partnerships (LLPs), and others) an S-Corporation, if formed properly, maintained properly, and run properly, can confer significant protection of personal assets against business liabilities.

Avoid Double Taxation: Again like many other businesses (except for the C-Corporation), an S-Corporation allows for the avoidance of the double taxation characteristic of C-Corporations, in which earnings are taxed once at the entity level, and again as dividends to the shareholders. The resulting “compound” tax rate on a C-Corporation’s earnings is higher than that achieved through most other entities.

Reduce Payroll & Medicare Taxes: Largely Unique to an S-Corporation is the ability to reduce Payroll & Medicare taxes, by classifying a portion of the corporation’s income as wages and another portion of the corporation’s income as a distribution. The portion that is classified as a distribution will not be subject to Payroll or Medicare Taxes – in contrast, being classified as a sole proprietor, disregarded, etc. is likely to result in the entire income being subject to self-employment taxes.

Simple Ownership Transfer: This is sort of a “turn the frown upside down” factor – an S-Corporation may only have one class of shares, so the transfer of ownership is easier. Additionally, an S-Corporation may not need to make basis adjustments to its property or comply with various potentially-complex accounting issues as a result of such a transfer.

* list is not exhaustive or exclusive

But, it’s not all roses.

Not only is an S-Corporation a relatively restrictive entity – if you don’t qualify for the rules, your S-Election can be “busted” and you’ll be diverted into a C-Corporation classification by default – but also it has certain characteristics that can be serious downsides, depending upon circumstances

Here are a few* potential downsides and restrictions of an S-Corporation:

“Phantom” Income:

Limit on Payroll Exclusion

The Corporate Form

Limits on Shareholders

* list is not exhaustive or exclusive

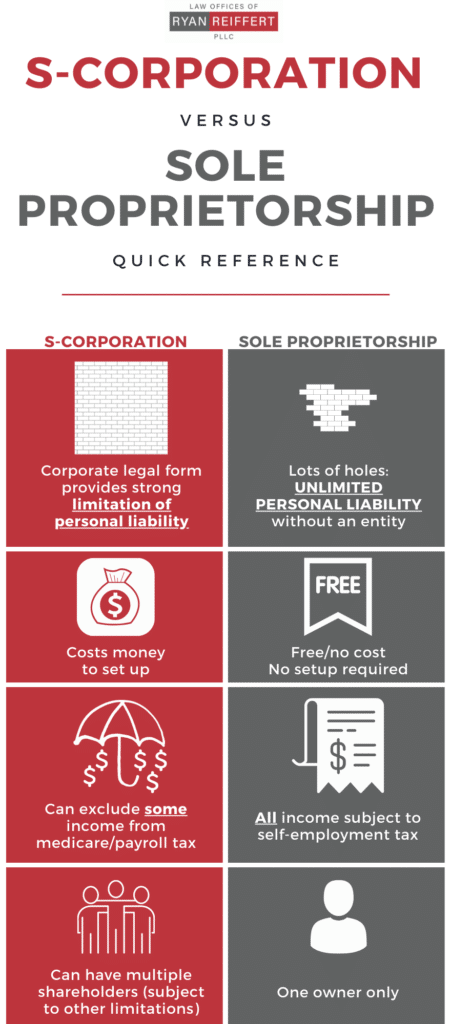

The below infographic summarizes some of the benefits and downsides discussed above, against the sole proprietorship as a point of comparison. Keep in mind that other comparisons (against LLCs, Limited Partnerships, etc.) are possible and relevant.

Infographic summarizing some benefits and drawbacks of S-Corporations

There are some other limitations on making an S-Election that are important to make you aware of – specifically, there are only three times that you may make an S-Election for your corporation by filing Form 2553.

First, you can file your Form 2553 any time during the two and a half months (actually, two months and 15 days) after the beginning of the tax year the election is to take effect. So, if your tax year begins on January 1, you have until March 15 to make your S-Election.

Second, you can file your Form 2553 any time during the first two and a half months (actually, two months and 15 days) of your corporation’s existence for it to take effect during the first tax year – and actually, this is sort of the same thing as the above, if you think about it, but the tax year is just a lot shorter. So, therefore, if you form your corporation during a half tax year… let’s say June 1, then you have until August 15 to make your S-Election.

Third, you can file your Form 2553 any time during the year, in order to have it take effect in the following tax year. So, for example, if your tax year starts on January 1, you can make an S-Election any time before March 15 for the current year, or any time after March 15 for the following year.